1. The Macro View: A Market Reaching Full Maturity

What began nearly 25 years ago as a basic utility for peer-to-peer transfers has matured into a sophisticated global financial ecosystem. Today, mobile money is no longer a niche service for the unbanked, it is a primary engine of the global economy, fundamentally reshaping how billions manage their financial lives.

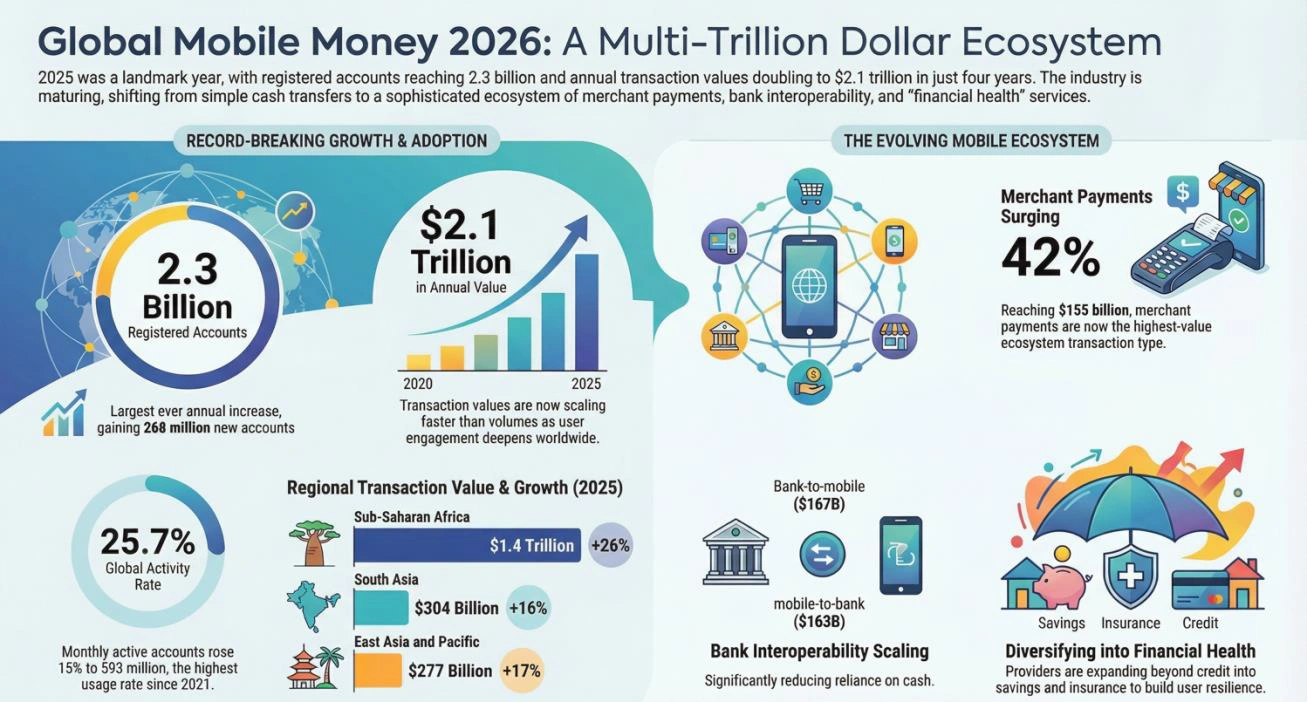

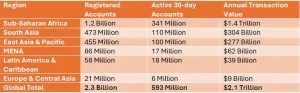

The sheer scale of this evolution is staggering. In 2025, the industry reached a landmark 2.3 billion registered accounts, bolstered by a record breaking 268 million new accounts added in a single year, which is the largest annual increase in history. With a global monthly activity rate now at 25.7%, the ecosystem has achieved a level of stickiness that was once the sole domain of traditional banking.

The velocity of this growth is perhaps the most significant indicator of a shifting paradigm. This milestone represents a “value-volume decoupling” where the depth of usage is now outstripping the sheer scale of adoption. While it took the industry 20 years to reach its first $1 trillion in annual transaction value, it took only four years to double that figure, with total value surpassing $2.1 trillion in 2025.

For providers, this transition from customer acquisition to high-frequency engagement is the primary driver of operational sustainability.

Global Mobile Money Performance by Region (2025)

This aggregate growth is increasingly defined by a fundamental pivot in transaction typologies, moving away from simple fund transfers toward complex, high-velocity digital commerce.

2. The Ecosystem Pivot: From Peer Transfers to Merchant Dominance

The strategic center of gravity has shifted from a P2P-centric utility to an Ecosystem-centric model. Merchant payments have emerged as the new engine of liquidity, allowing capital to circulate within the digital envelope rather than leaking out as physical cash. This digitalization of cash is evidenced by the $0.76 cash-out ratio recorded in December 2025. The remaining $0.24 delta represents Retained Digital Liquidity, i.e. the value that remains in the ecosystem to be recycled through digital services, significantly enhancing the velocity of money.

Merchant payments were the industry’s most explosive use case, surging 42% to 155 billion. In a significant shift for the digital economy, merchant payments have now surpassed bulk disbursements (139 billion) to become the highest-value ecosystem transaction type. This growth was concentrated in high adoption corridors:

• East Africa: The primary global engine, fueling 75% of total merchant payment growth.

• South Asia: Contributing 10% of the growth share.

• Southeast Asia: Accounting for 7% of the growth.

Interoperability is the invisible hand guiding this transition. Bank-to-mobile flows reached $167 billion, closely mirrored by $163 billion in mobile-to-bank transfers. This bidirectional harmony suggests that mobile money is no longer a separate silo but an integrated layer of the broader financial architecture. As transactional utility evolves into everyday spending, the industry is increasingly focused on the higher margin frontier of holistic financial health.

3. The Financial Health Frontier: Credit, Savings, and Microinsurance

The industry is moving beyond the access narrative toward financial health, i.e. the ability of users to manage shocks and invest in their futures. Adjacent services are the primary drivers of this evolution, transforming the mobile wallet from a storage device into a sophisticated financial dashboard. This diversification has catalyzed a 15% rise in Average Revenue Per User (ARPU), which climbed from $1.52 to $1.75. For the global investment community, the fact that 80% of providers have reached EBITDA positive sustainability drastically lowers the risk profile for Foreign Direct Investment (FDI) in emerging fintech sectors.

The three pillars of these adjacent services are maturing rapidly:

• Credit: Nano-loans (under $20) dominate the landscape, offered by 79% of providers. The integration of AI/ML for credit scoring exemplified by the Orange Money and JUMO partnership allows for real-time underwriting of the historically unbanked.

• Savings: There was a 31% rise in unique customers transferring funds to savings accounts. Tools like MTN’s Yinvesta in Uganda demonstrate the demand for micro-investment vehicles that offer daily interest on small balances.

• Insurance: This was the fastest growing adjacent service, with a 33% increase in providers. However, a massive protection gap persists. Only 12% of the 3 billion people in the target market are currently covered by a policy, representing a significant untapped commercial frontier.

While the commercial outlook is robust, the industry must now navigate rising regulatory friction and the mounting costs of systemic fraud.

4. Navigating the Headwinds: Policy, Taxation and the Fraud Challenge

The regulatory environment is currently the most volatile variable in the industry’s trajectory. As mobile money scales, it faces dual pressures, the need for enabling frameworks (KYC, interoperability) and the mounting fiscal appetite of governments seeking to expand revenue bases.

The Taxation Conflict Sector – specific taxes continue to create regressive friction. The most high-profile case remains Ghana’s E-Levy, which, after failing to meet revenue targets and stifling adoption, was officially repealed in April 2025. Despite this lesson, other markets have introduced similar measures:

• Zambia: Implemented a per-transaction levy on P2P transfers.

• Benin: Introduced a 1% tax on large cash payments.

• Mali: Enforced a 1% withdrawal tax.

• Senegal: Signalled new taxes on transfers and merchant payments.

The Fraud Typology – as transaction values scale, so does the sophistication of criminal actors. Industry data highlights a high prevalence of specific fraud types:

• Identity Fraud (90%) and Social Engineering (88%) remain the dominant threats.

• Insider Fraud (87%) represents a persistent internal structural risk.

• SIM Swap Fraud followed at 79%.

In response, leaders like Safaricom and Airtel have deployed AI-driven mitigation strategies to analyze transaction anomalies in real-time. Yet, beyond technical security, the psychological cost of fraud remains a primary barrier to inclusion, particularly for marginalized demographics.

5. The Inclusive and Sustainable Future: Gender Gaps and Climate Finance

Achieving total market penetration requires addressing the widening gender gap and leveraging mobile money for climate resilience. These are no longer just social goals, they are commercial imperatives for the next billion users.

The Widening Gender Gap – a commercial failure in a concerning regression, the gender gap in account ownership in Low and Middle-Income Countries (LMICs) has widened. Women are now 36% less likely than men to own an account, a significant increase from the 30% gap recorded in 2021. The four primary barriers to closing this gap include:

• Awareness: Disproportionately lower among women in South Asia and MENA.

• Relevance: A persistent, culturally rooted preference for cash.

• Knowledge/Skills: Gaps in digital financial literacy and handset confidence.

• Social Norms: Specifically, family disapproval in conservative markets.

Climate Finance as the New Frontier – mobile money is evolving into a critical infrastructure for climate adaptation. Through Pay-As-You-Go (PAYG) solar partnerships (e.g., MTN Zambia/Sun King), mobile money is providing clean energy to the off-grid. Even more transformative is the Cook-to-Earn model (pioneered by ATEC), which utilizes IoT enabled stoves and mobile wallets to channel carbon credit revenues directly to users. This shifts the user’s role from a passive consumer to an active participant in global carbon markets.

6. Strategic Conclusion: Priorities for 2026 and Beyond

As we move toward the 2030 horizon, the priorities for the mobile money industry must focus on three executive pillars:

• Cross-Border Harmonization – aligning regulatory and KYC standards across regions like the EAC and AfCFTA to lower the cost of remittances, which still averages 8.78% in Sub-Saharan Africa.

• Literacy as Risk Mitigation – digital financial literacy is now a prerequisite for the safe adoption of adjacent services and a critical defense against fraud.

• Digital Public Infrastructure (DPI) Integration – positioning mobile wallets as the last-mile for government services and digital identity.

Crucially, as the sector digitalizes the Agent Network (30 million registered agents) remains the industry’s most indispensable asset. The Ratio of Attention, which is the average number of active 30-day accounts per agent has fallen from 28:1 to 19:1. This indicates that agents are becoming more accessible, providing the necessary human touchpoint to build trust among the underserved.

The future of mobile money lies in this hybrid balance of the sophisticated efficiency of AI and the enduring trust of the human network.